Shutthiphong Chandaeng

Intro

Web personal privacy is a raving issue at the minute for lots of web users worldwide, and one threat point is making use of third-party cookies for tracking and information collection. While declared to be safe and individualized for your own tastes, lots of feel that it is incorrect for big corporations to benefit from our individual info, tastes, and choices. Then integrated with individual determining info and other cybersecurity dangers, a brand-new pattern has actually been developed where we might go into a cookie-free world. Sadly, absolutely nothing comes free of charge, and digital services desire their reasonable share of marketing incomes, and marketers would like to know their advertisement invest is in fact causing sales.

Since early 2024, the main advocate of a no-cookie world is Apple ( AAPL) and they supply an intricate Intelligent Tracing Avoidance function for users. A lot of other advertisement platforms have actually been reluctant, particularly Google ( GOOG), as they have actually tried to stall mentioning “screening” or “experimentation” with more protected cookie innovation. Nevertheless, the reaction continues and a current statement validates that even Google Chrome will now be restricting tracking, and might even completely stage out third-party cookies So what can marketers do now that their high-value consumer tracking and intake information source is drying up? Well, one prime chance depends on a little, choose group of ad authenticators. I think that DoubleVerify ( NYSE: DV) is the main prospect for financiers wanting to take advantage of a higher-quality ad landscape.

Marketers suggested that ‘several internet browsers phasing out third-party cookies’ was their main concern. This concern held the leading area in 2022, and increased from 38.5% to 45.1% in 2023, revealing the high significance of internet browser choices as the market gets ready for cookie deprecation.

– DoubleVerify Post-Cookie Study Report

DoubleVerify is a newbie to the growing online marketing market however is discovering a specific niche in offering authentication services for marketers. Particularly, the business offers third-party confirmation of where advertisements are seen, by whom, and the effect of the advertisements. The primary advantage of DV is the capability to be platform agnostic, and the business will be successful no matter which marketing platform triumphes, such as Google, Meta ( META), Amazon ( AMZN), The Trade Desk ( TTD), or more.

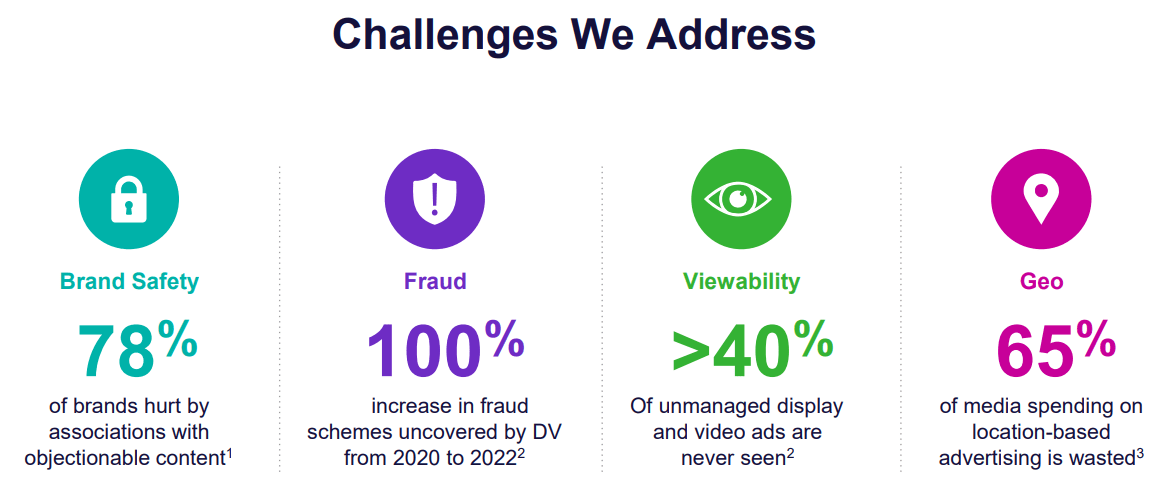

Then, as the info highway closes down due to an absence of third-party cookies, DV will be among the only relied on partners in between marketers and publishers for which insights and authentication can be validated. Likewise, in an age where marketers deal with threat from associations with objectionable material, scams, bad viewership, and unoptimized geolocation, DV has several successful courses for long-lasting development. As such, I think this little, however economically sound, business is among the premier financial investments in the marketing market.

DoubleVerify Financier Discussion

The Advertisement Market is Substantial

Marketing is among the biggest markets on the planet, however there is still huge chance for enhancements now that we have actually transferred to a digital age. Numerous concerns are based upon this brand-new digital environment, and DoubleVerify has actually discovered a strong specific niche to turn into. This assists to balance out weak point in the face of a higher-than-normal quantity of competitors. A lot of DV’s services are best-in-class, however elements of each can be executed by advertisement publishing platforms and markets. This is why marketers represent 90% of overall incomes, and combinations with publishers will be essential for long-lasting success. As management states in the Post-Cookie Study Report, “DV is happy to gear up both sides of the market with tools and services that cultivate a more transparent method of working.” The secret is whether the cash circulation stays practical.

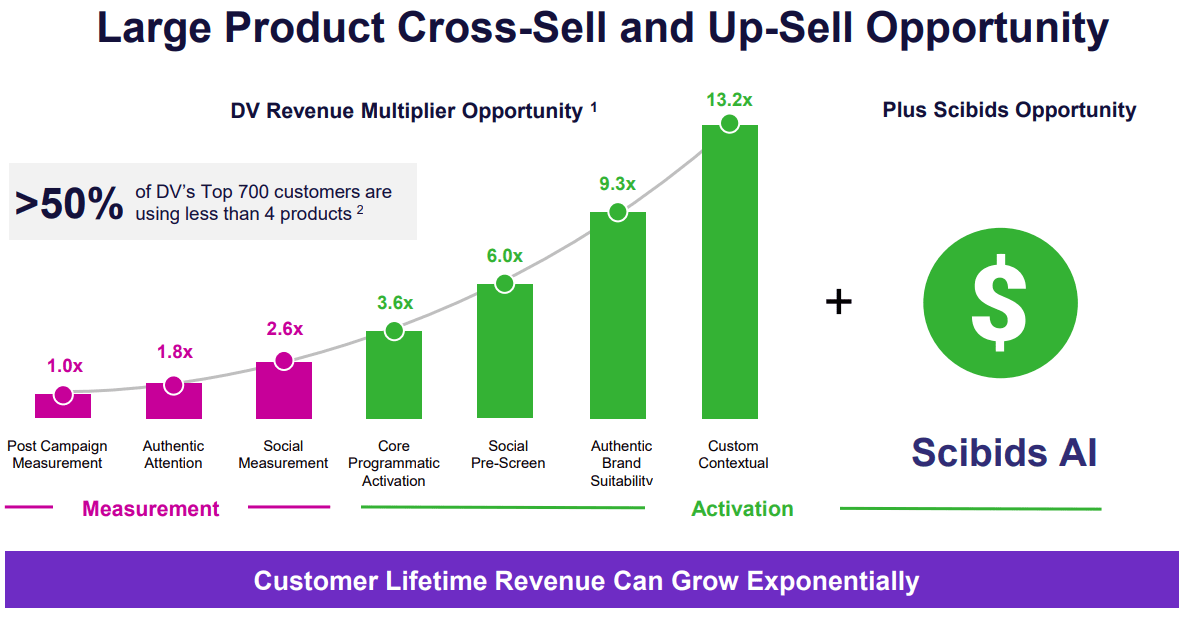

DV essential offerings are a suite of services that provide a bolt-on technique for customers based upon use. And, the majority of DV’s success has actually been based upon maintaining consumers and moving them towards greater income costs chances. As an example, management anticipates that consumers who utilize the entire suite of tools, or 7 services throughout measurement and activation, pay up to 13x more incomes in general. As such, incomes have actually had the ability to substance over 30% annually because its starting in 2008. New chances continue to be presented too, consisting of AI services thanks to the acquisition of Scibids in 2015. As explained by an AdExchanger post:

‘ Scibids dynamically changes quotes for every impression based upon a marketer’s KPIs, such as viewability or wanted CPM variety. To notify its choices, Scibids pulls info through APIs from demand-side platforms, consisting of first-party information and media expense, along with attention information from DV.

‘ It simply takes our information and moves it to a totally various level of granularity and applicability for our consumers,’ DV CEO Mark Zagorski informed AdExchanger.

‘ For instance, DV can utilize the Scibids tech to produce more refined sections for media activation, recognize high-attention stock and enhance projects without depending on third-party cookies by representing variables such as domain positioning, gadget and geolocation.’

DoubleVerify Financier Discussion

Quantitative Assistance Elements

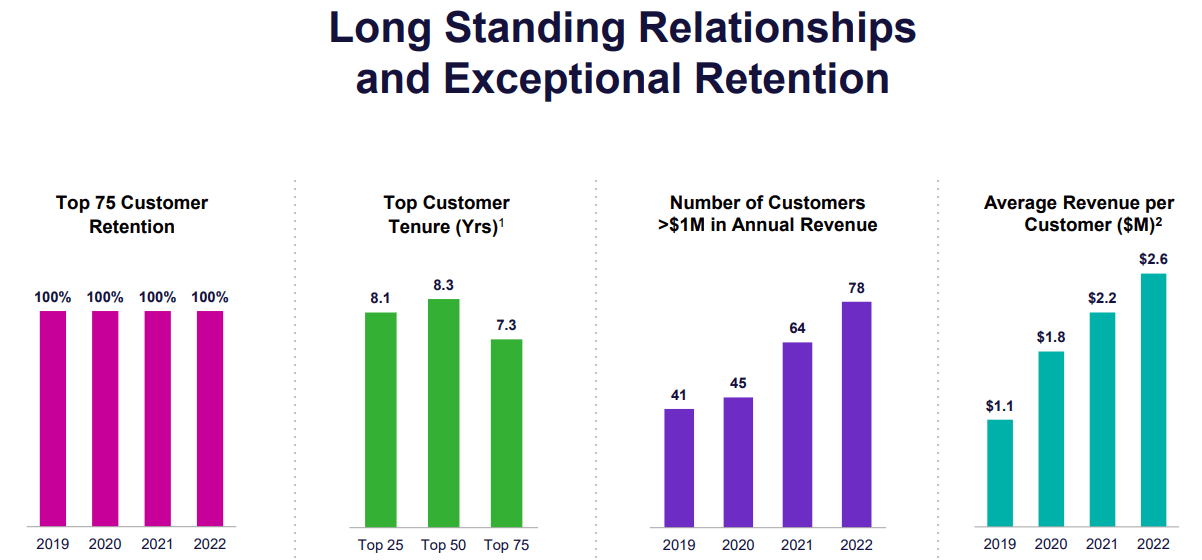

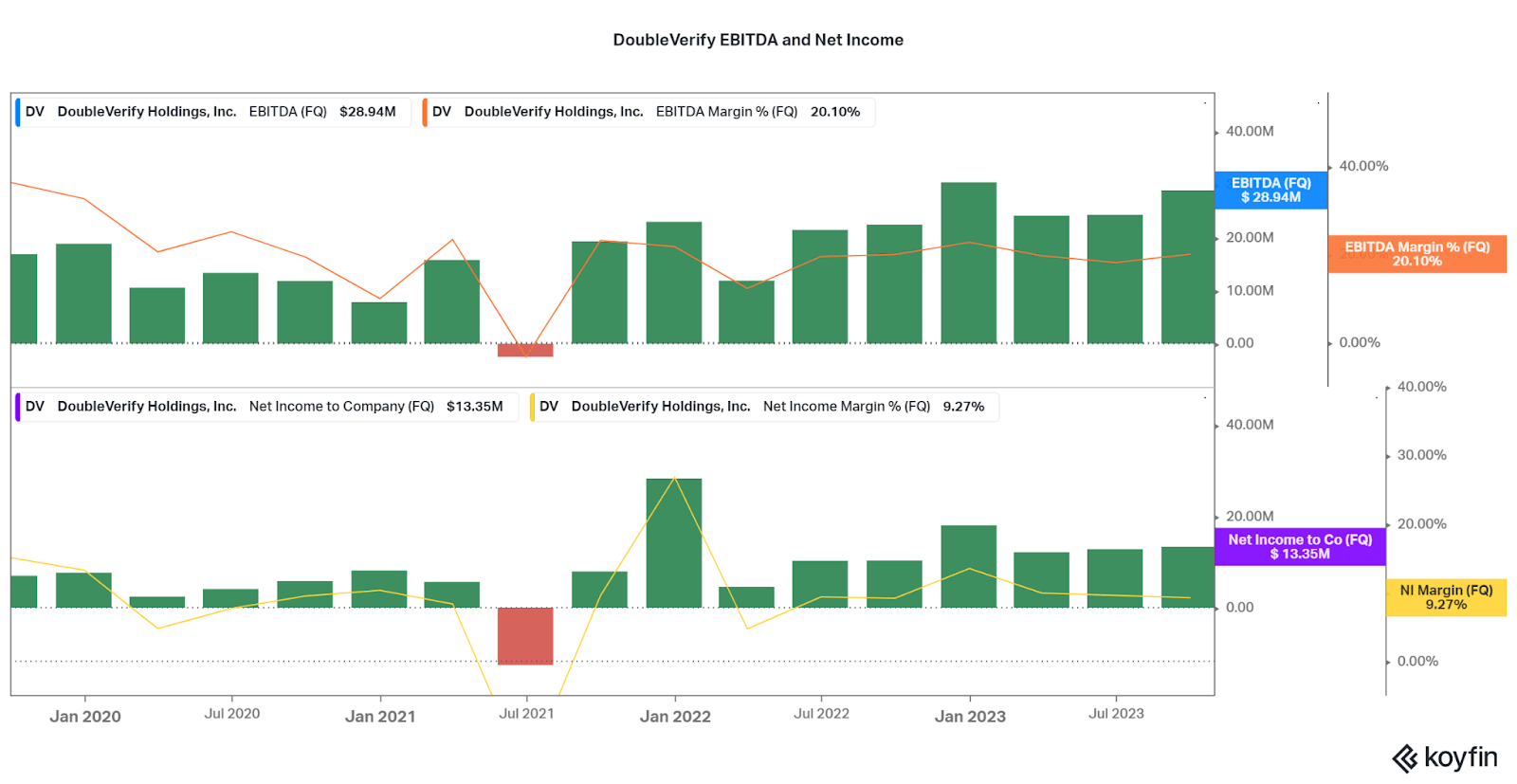

So while DoubleVerify still has time to establish a moat and fend off competitors, it will be necessary to utilize the monetary information as evidence of success. So far, they provide lots of information points that recommend success. Initially, DV is establishing strong relationships, and this appears by the 100% retention rate of leading 75 consumers. Likewise, these consumers have actually been partnered for several years, with a typical period of over 7 years. At the exact same time, the typical income per consumer has actually increased from $1.1 million in 2019 to $2.6 million in 2022. As both the variety of consumers and typical invest continue to increase, I am positive that the platform is working. Existing net income retention is at 127% for 2022, and I anticipate this rate to continue for a long time regardless of a downturn in development over the previous year due to a weaker advertisement market.

DoubleVerify Financier Discussion

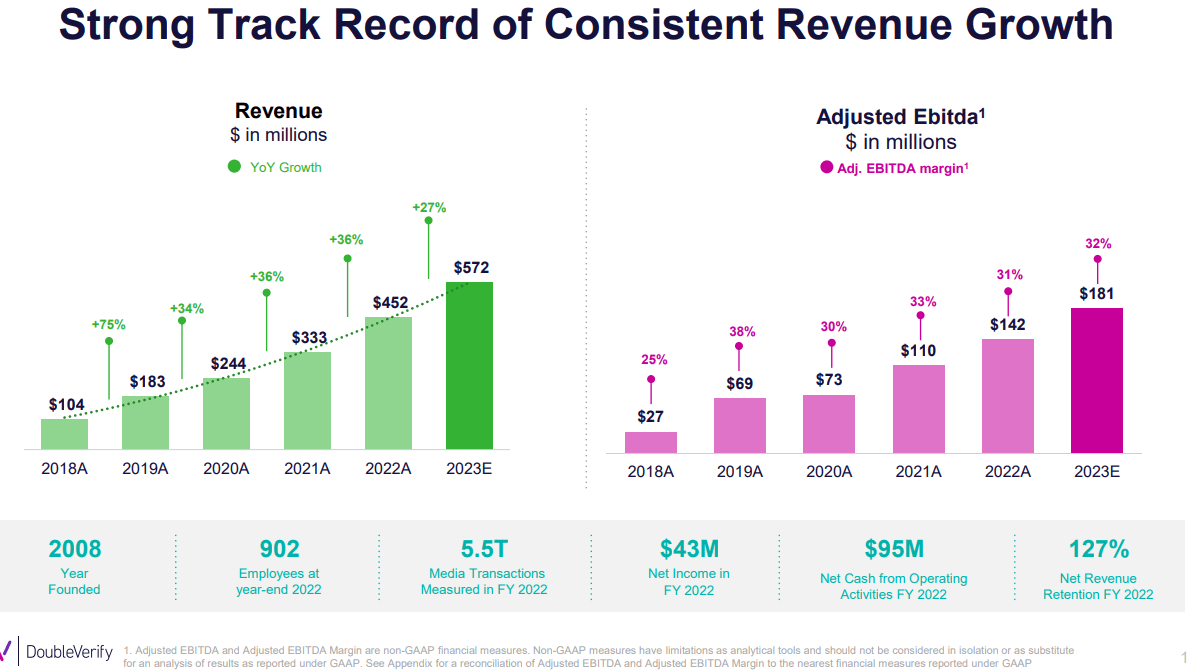

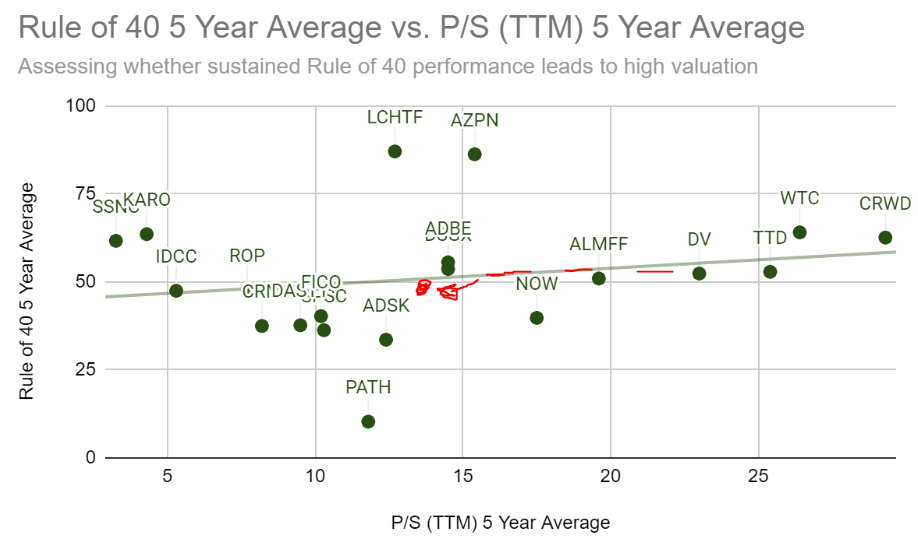

At the exact same time, the majority of tech financiers understand that natural development is not the just essential element. Rather, success is what sets out the very best from the rest. To that point, DoubleVerify needs to be kept in mind as exceptionally successful for its size and development rate. In reality, the business is beating the Guideline of 40 at 46% (tracking rev development and EBITDA margin). When taking 5-year averages into factor to consider, DV is even much better at 52%. While income development is not to an incredible level, the typical 34% rate is adept.

At the exact same time, EBITDA margins are favorable around 17-20%, and Earnings is likewise favorable, albeit irregular. I can not indicate other development peers that provide such levels of success, even market stalwarts such as WPP ( WPP) and TTD. In specific, the primary competing Important Advertisement Science Holding Corp. ( IAS) is growing slower, less successful, and more leveraged. As such, I think that the financials show the strong chance that is offered for DoubleVerify.

DoubleVerify Financier Discussion Koyfin

Conclusion

I think that DoubleVerify is presently in an excellent position to turn into a leader in advertisement authentication for the broadening digital advertisement age. I likewise think that DV’s present evaluation makes it the much better option when compared to The Trade Desk. Why? Well initially DV is growing incomes at about the exact same rate as TTD however is more successful on the bottom line (both EBITDA and earnings margins). So for more money generation, one would believe that DV is valued greater, however this is likewise not so. TTD stays among the more exceptionally valued business in the market at a 150x EV/EBITDA and 19x P/S all while DV is presently trading at 55x and 12x, respectively. For me, that suffices of a distinction to make DV stick out and be the only practical chance at the minute.

Author. Utilizing Looking For Alpha Data.

DoubleVerify might do not have the promotion of others in the marketing market, however this does not imply that the evaluation will stay listed below peers. The concern is that till then, the financial investment stays dangerous however bearable for long-lasting financiers such as myself. With this volatility, I think that financiers building up shares anywhere in between $30-$ 35 per share will enjoy in the years to come. At the exact same time, as the advertisement market supports after a recession through 2023, appraisals might increase once again. For that reason, it can be anticipated that the share cost might increase and $35-$ 40 stay practical build-up levels. That is what I will be attempting to do through 2024.

Thanks for reading. Do not hesitate to share your ideas listed below.